The Autumn Budget 2025 unveiled a series of VAT changes for UK businesses that must be understood and planned for ahead of the 2026 rollout. These updates impact how companies handle charitable donations, price private hire services, issue VAT invoices, and manage international group structures. While some changes aim to modernise reporting and reduce administrative burdens, others are part of wider HMRC VAT reforms announced in autumn budget documents aimed at closing long-standing tax gaps and increasing compliance.

At Apex Accountants, we help businesses across the UK interpret complex tax changes and apply them with confidence. Our experienced advisors provide tailored VAT guidance, system reviews, and ongoing support to keep your business compliant and prepared. With several deadlines approaching, VAT planning after 2025 budget announcements is now essential for businesses that want to avoid penalties and stay ahead.

In this article, we explore the most significant VAT changes announced in the Autumn Budget, answer the questions business owners are now asking, and explain how to prepare for what’s ahead.

Can my business donate goods to charity without paying VAT?

Yes. From 1 April 2026, VAT will no longer apply to eligible business donations of goods to UK-registered charities.

This relief applies to:

- Goods valued up to £100 per item

- Essential electrical items up to £200 (e.g., laptops, fridges)

Only registered charities qualify. CICs and social enterprises are excluded unless they register as charities.

Previously, VAT rules created a barrier to donating stock. This reform makes it easier for businesses to support charitable causes while reducing waste. Apex Accountants can review your donation records and ensure all qualifying conditions are met.

Will private hire and taxi operators have to charge full VAT?

Yes. From 2 January 2026, VAT-registered private hire vehicle (PHV) and taxi operators will be required to apply 20% VAT to the full fare.

This amendment follows the removal of eligibility for the Tour Operators’ Margin Scheme (TOMS). The rule applies if you contract as a principal rather than an agent. In London, operators are already required to act as principals. In other areas, the situation depends on how your contracts are structured.

If your firm operates across different regions, Apex Accountants can assess your booking flows and advise whether a contract review is necessary.

What VAT changes apply to the Motability Scheme?

From July 2026, VAT and Insurance Premium Tax (IPT) reliefs for the Motability Scheme will be limited to essential mobility needs.

The following will remain VAT-exempt:

- Weekly lease payments funded by welfare benefits

- Vehicles adapted for wheelchair or stretcher users

- Resale of vehicles under the scheme

Apex Accountants can help you identify which parts of your leasing or pricing model are VATable and restructure your documentation accordingly.

Do all VAT-registered businesses have to switch to e-invoicing?

Yes. From April 2029, all VAT-registered businesses must issue structured electronic invoices for B2B and B2G transactions.

This reform doesn’t change the VAT rate but does change how invoices are formatted, sent, and stored. A full technical roadmap will be published in Budget 2026.

If your business relies on manual or PDF-based invoicing, you should begin preparing now. Apex Accountants can help you choose compliant software and build the transition into your wider VAT planning after 2025 budget preparations.

How will VAT grouping rules change for UK businesses with overseas branches?

From 26 November 2025, the UK will revert to the “whole establishment” principle for VAT groups.

This means intra-entity services between UK head offices and overseas branches in the same VAT group will no longer trigger VAT. The update also applies if the overseas branch is in an EU country that does not follow whole-entity grouping.

This move reverses the VAT treatment introduced after the Skandia case. If your business has overpaid VAT since 2016 on internal services, Apex Accountants can help you file a correction and reclaim the overpayment.

Who is responsible for VAT on unreturned deposits in Deposit Return Schemes?

From October 2027, the central deposit management organisation will account for VAT on unreturned deposits under the UK’s deposit return scheme (DRS), instead of individual producers.

This simplifies VAT administration for producers and retailers involved in the scheme. Apex Accountants can help ensure your VAT processes align with this change ahead of the rollout.

Has the VAT registration threshold changed?

No. The VAT registration threshold remains frozen at £90,000.

As inflation increases turnover, more small businesses will pass the threshold even if profits stay flat. Late registration can lead to penalties and backdated VAT bills.

Apex Accountants can monitor your turnover, advise on early registration, and assist with all compliance steps linked to HMRC VAT reforms announced in Autumn Budget guidance.

How Our Services Help You Prepare for VAT Changes for UK Businesses

Apex Accountants offers a full suite of VAT services tailored to the needs of UK businesses.

Our VAT support includes:

- VAT planning, compliance, and advisory

- E-invoicing system integration and rollout

- VAT treatment guidance on donations, PHVs, leasing, and digital services

- Cross-border VAT group structuring and corrections

- Sector-specific VAT support for charities, transport, and retail

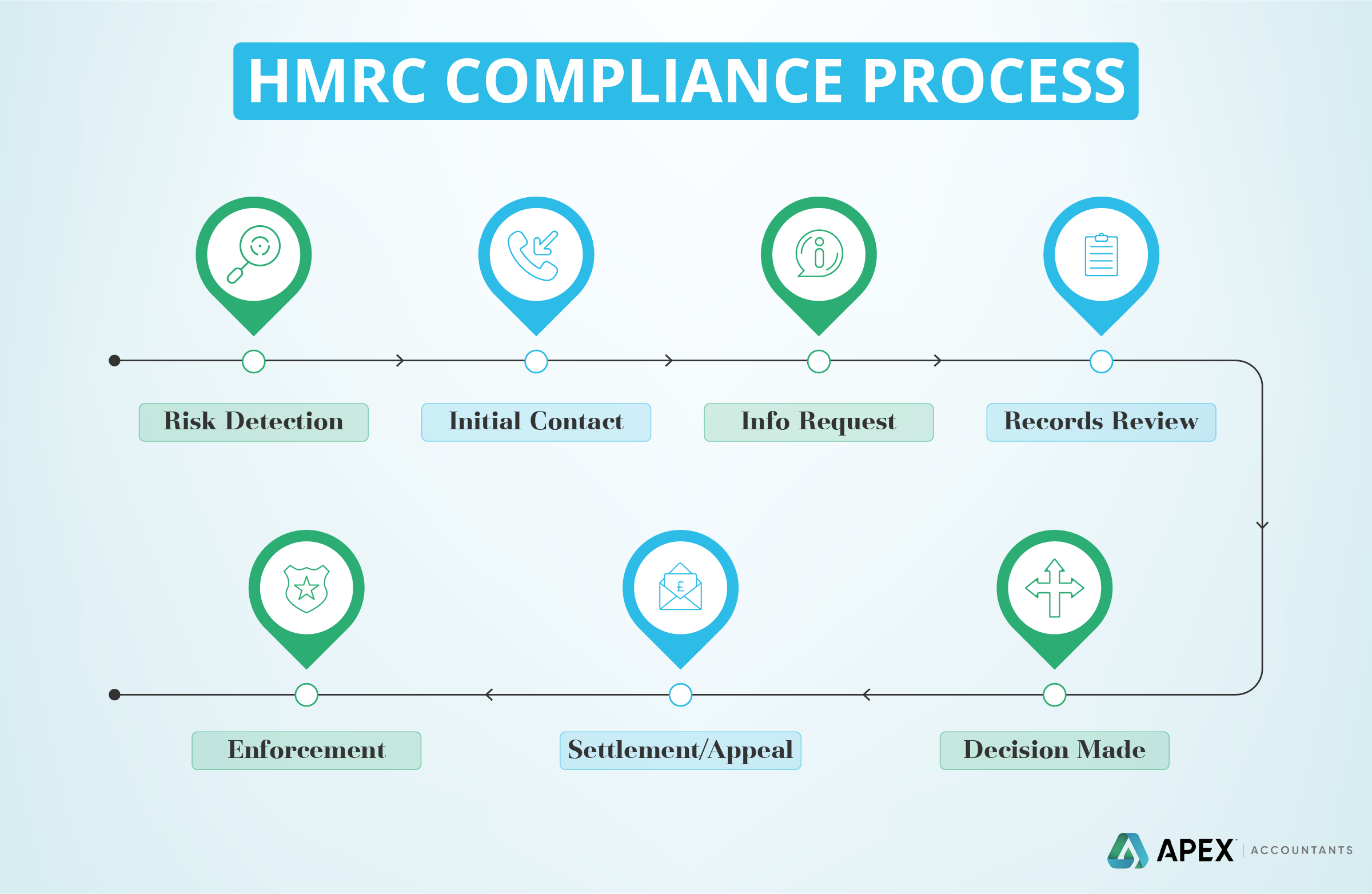

- Representation and submission support during HMRC reviews or disputes

We help businesses stay compliant, reduce tax risk, and prepare well in advance of regulatory changes. Whether you’re restructuring PHV fares, planning for e-invoicing, or reviewing donation procedures, Apex Accountants is here to support you every step of the way.

Contact us today to speak with a VAT advisor and receive tailored guidance for your business.